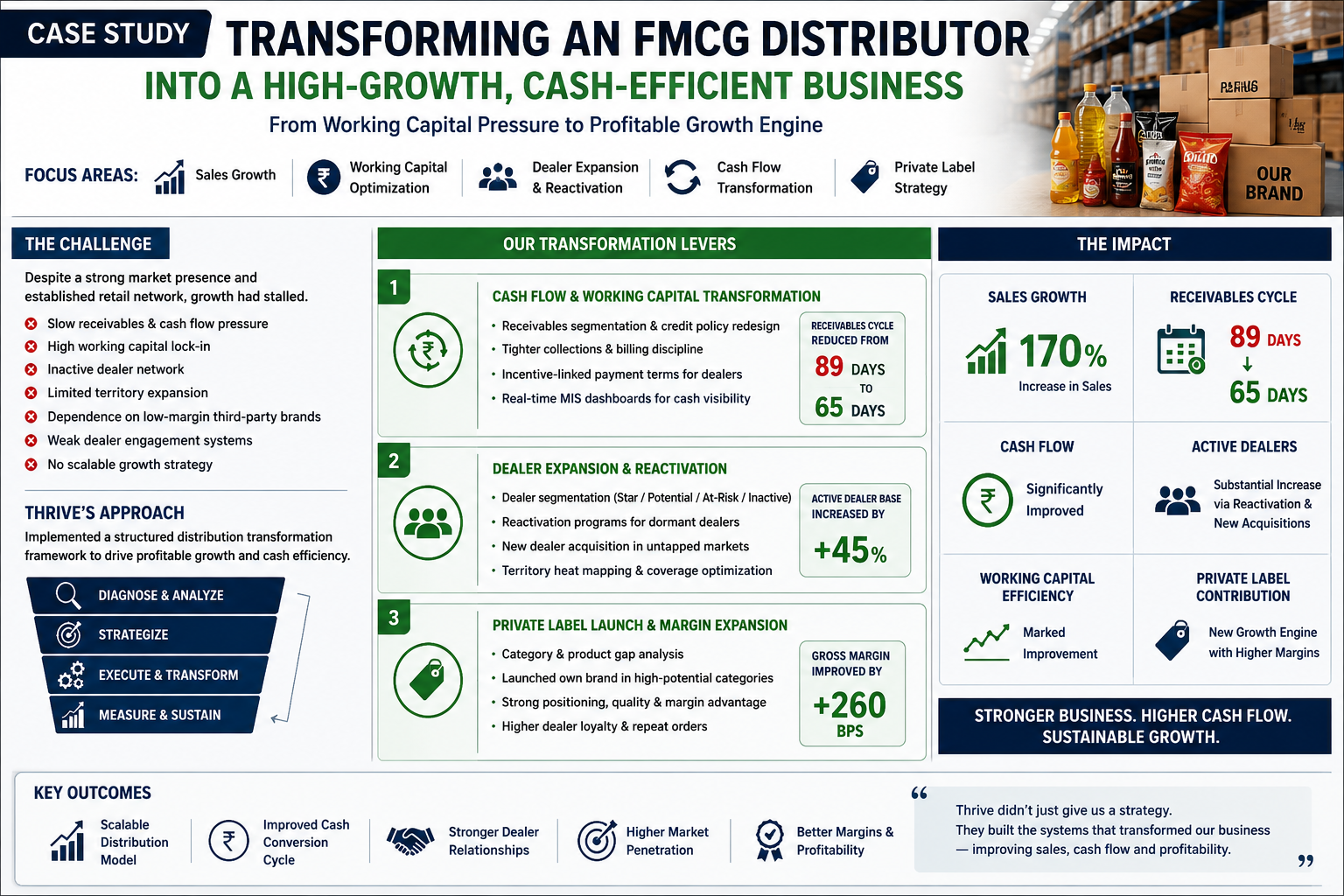

FMCG Distributor: Improved cash flow & sales by 170%

Focus Areas

Sales Growth | Working Capital Optimization | Dealer Expansion | Cash Flow Transformation | Private Label Strategy

The Challenge

This FMCG distribution company had a solid reputation and strong retail network, but their growth had hit a wall.

Demand wasn’t the problem. What really slowed them down were structural issues:

- Receivables were coming in slowly, so cash flow was always tight.

- Way too much working capital got stuck.

- Lots of dealers just weren’t active.

- They barely expanded into new territories.

- Most sales came from third-party brands with really low margins.

- Dealer engagement systems were weak.

- There was no real growth strategy that could scale.

Revenue held steady, but if you looked closer, profits and cash efficiency always felt squeezed.

Thrive’s Strategic Approach

Thrive came in with a clear plan — rework distribution from the ground up. The focus? Working capital, dealer network, faster sales, better channel productivity, higher margins, and private label growth.

This wasn’t just about bumping up sales numbers. Thrive wanted to build a business that could grow, scale, and actually get stronger financially.

- Working Capital & Cash Flow Transformation

First, Thrive dug into everything money-related:

- How quickly receivables came in

- Dealer payment habits

- Credit exposure

- Inventory movement

- Product profitability

- How working capital got deployed

Receivables Segmentation Model

They broke dealers into groups based on payment behavior, purchase consistency, credit risk, volume, and collection efficiency. With this, they set up smarter credit policies and tighter controls over cash flow.

Working Capital Efficiency Framework through AI

Thrive revamped credit cycles, streamlined collections, pushed for billing discipline, redesigned dealer incentives, and fixed inventory planning. Created an AI-based automated cash collection system that helped to reduce the credit cycles dramatically.

Impact:

- Receivables cycle dropped from 89 days to just 65

- Cash flow became much clearer

- Working capital got way more efficient

- Less need to borrow from outside

- Cash conversion happened faster

In the end, the company ran leaner and got financially stronger.

Dealer Expansion & Reactivation Strategy

Thrive spotted gaps — territories weren’t covered, dealer productivity was low, penetration was weak, and retail activation lagged.

Key Moves:

Dealer Reactivation Program

Thrive targeted inactive dealers and brought them back using incentives, structured engagement, faster supply, and retail support.

New Dealer Acquisition

They mapped territories to find untapped micro-markets, pushed into tier 2 and 3 regions, and homed in on clusters with high retail potential.

Impact:

- More active dealers onboard

- Stronger presence across territories

- Faster sales at both primary and secondary levels

- Better coverage among retailers

Private Label & Margin Expansion

Launching the company’s own FMCG brand totally changed the game.

Thrive helped with everything from picking the right categories and analyzing margins to planning GTM strategies, packaging, positioning, and launching through distributors.

Strategic Rationale

Selling third-party products was good for scale, but margins stayed thin. Private label brought higher gross margins, stronger dealer loyalty, more control on pricing, and boosted the long-term value of the business.

Impact:

- Margins jumped across the board

- Profitability mix improved

- Dealer engagement strengthened

- More control on how the brand showed up in the market

- Created a whole new growth engine outside the traditional distribution

Business Outcomes

Metric Before Thrive After Transformation

Sales Growth Stable Increased by ~170%

Receivables Cycle 89 Days 65 Days

Working Capital Efficiency Weak Significantly improved

Dealer Network Fragmented Expanded & reactivated

Product Strategy Third-party only Private label launched

Margins Low Improved blended margins

Strategic Impact

The company went from a traditional distributor to:

- Cash-efficient business

- Scalable platform

- Higher-margin, brand-led organization

- Ready for aggressive market expansion

And — most importantly — it didn’t just grow sales. It boosted the financial quality of that growth.

The Thrive Difference

Most consultancies chase sales alone.

Thrive does more: they care about quality of growth, cash flow efficiency, working capital, channel scalability, margin expansion, and building long-term value.

By blending sales transformation with real financial discipline, Thrive helped the company unlock growth that’s both profitable and sustainable.